The Paradox of Dollar Strength: Has the Market Given Up All the Reasons to Rise?

Peyman Molavi | economist

We are now at the peak of the dollar’s power. The dollar should have fallen after the peace deal, reversing safe-haven flows and capital outflows from U.S. assets. Instead, the first Fed meeting under Warsh fundamentally changed market expectations and reinforced the notion that U.S. monetary policy will remain tighter for a longer period of time.

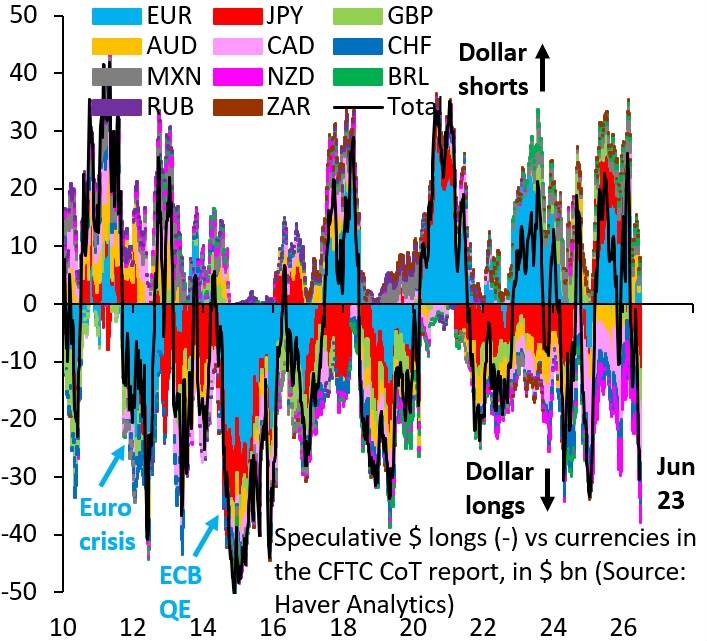

As a result, speculative positioning has shifted sharply to dollar longs, creating one of the busiest trades in global markets. But history shows that extreme positioning rarely signals the start of a sustained trend – it often signals its maturity. When everyone is on the same side of a deal, the market becomes increasingly sensitive to even small changes in the underlying narrative.

A moderation in U.S. growth, a shift in inflation expectations, the resurgence of the attractiveness of non-U.S. assets, or even a subtle shift in the Fed’s communications can trigger a broad reassessment of dollar risk. In this environment, the same investors who fueled the dollar’s strength may become a source of its weakness by reducing their positions. From an asset management perspective, periods of peak confidence in a single macro narrative are often the moments when diversification matters most. The question is no longer whether the dollar is strong, but whether the market has factored in almost every reason for it to remain strong.